How are you Stock Market Proponents now?

General Topic

Stock market has dropped most EVERY day for over a month now. How are yall that were such huge proponents when i mentioned this 5-6 weeks ago? Still making plenty of money? I lost a bunch before i sold my Mutual Funds to buy some land. Fortunately my land is still worth as much today as it was last month. My Mutual Fund would have dropped by 15-20k if i had waited to sell until today for example. Glad i got out in time.

Glad I went to cash with some big stuff a month ago, and now have a pile waiting to drop back in after this settles down.

I'm down about 10% from my highs on stocks, which I'm pleased with considering the broader markets have fallen a bit more than that. I made plenty of gains in 2020 and 2021 to offset this correction. And, like Lou, I'm sitting on a nice pile of cash to put back into stocks when things settle down a bit.

I survived the 2000 dot com crash, the 2008 financial crash, and the 2020 covid crash. This minor correction is just a blip on the radar, and should be another opportunity to buy some great stocks at a discount, soon.

Matt

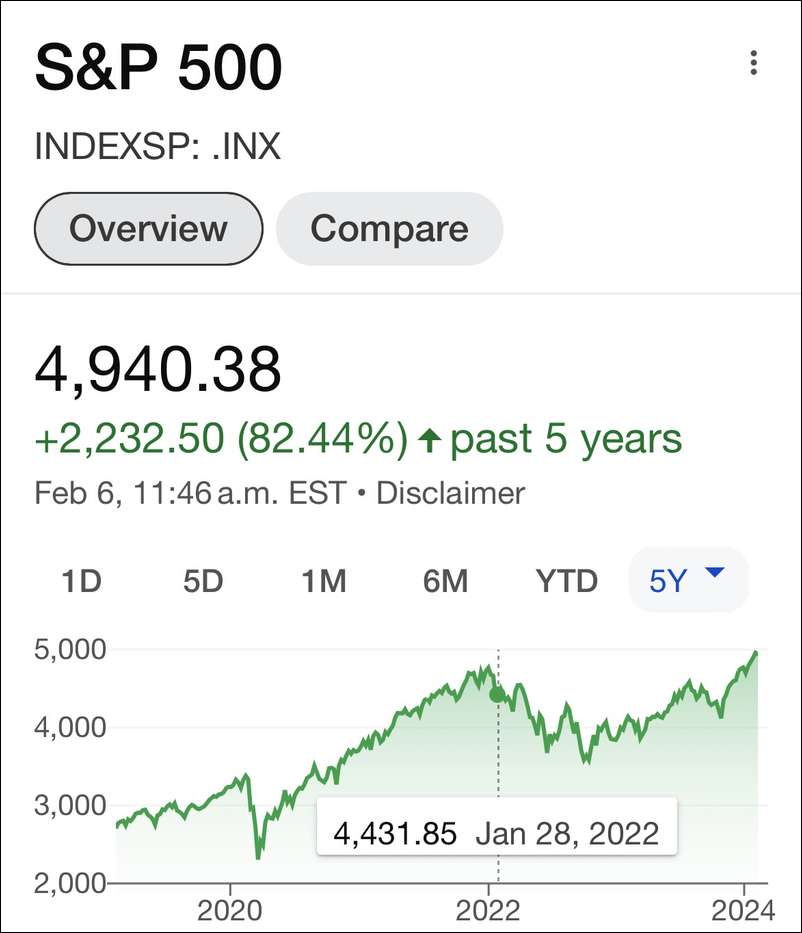

I’m feeling fantastic. The DOW is down about 5.9% this past month. The DOW is up 11% the past year and over 70% the past five years. If you are concerned about one month, or a few months or even a year, you should probably invest in a bank savings account or CDs and loose money every day, to inflation. Seriously.

Meh...I'm in for the long haul. Dips and peaks don't bother or excite me, strategy may change as I get older, but I likely won't notice this in 30 years. Hindsight is always 20/20, I'm still real estate heavy but stock market has it's place in my portfolio. S and P 500 is still currently up 15% over the last calendar year.

I max rothIRA's January 2 every year, this year it wasn't so great, but the 28% I got last year I would say I did ok. I'm still buying stocks and real estate. Maybe you are lucky and you got out in time. Or maybe it shifts again and you miss out on another 20% year. Nobody has the answer that, and if they tell you they do they're lying.

You only lose it if you sell. Keeping a lot of cash with the current rate of inflation doesn't interest me much, but to each their own.

I was thinking of calling Pelosi, i'm sure she has some great stock tips to give out to the general public.

Dollar cost average so it doesnt matter longterm.

Same with Bitcoin, dollar cost average

Just dollar cost average and keep at it every two weeks for 40 years and don’t look back. Buy land too!

401K

2021- Up 18.3% (and more than 1/3 of that gain was in January. Before the JB could impact much)

2022- down 11.94 for the year. But JB will turn it around on 1/31 ;)

2019 & 2020. Up 28% and 24% respectively.

At 56, don’t tell me the stock market isn’t the economy. (That is entitled loser talk)

I am regretting not parking a large chunk of money into a money market at the beginning of this month. Only regret it because the investments will be sold as we roll the money from a 403b into a 457, totally different plan with better investments and much lower fees. Could've sold high and bought back in lower. Otherwise I don't pay much attention.

I am 45 been consistently sticking money in the stock market for over 20 years. It is amazing what you can accumulate over that period of time. I most likely will retire in 4-5 years and never work another day in my life. The wife and I have never made what many would consider huge money, but both have done well over the years. Lived below our means and because of that and the stock market are in a nice position at this point in our lives. Not saying the stock market is the only way to make your money work for you. Guys do well in real estate and other areas. Also not saying buying a piece of land is a bad investment. It is hard to have a piece of land generate income for retirement or go up in value like same amount of money in the markets over the long term. Also you don't want to have to sell your land that you become very attached to and get enjoyment or of to fund your retirement.

My last two cents is diversify. Diversify what you have in the markets. Stocks, bonds whether mutual funds or individual stocks/bonds. Different sectors, small companies, large companies, US companies and over seas. Short term bonds/Long term bonds. No doubt sometimes the stock market is 2 steps forward and 1 step back. But if you really look it more like 3 or 4 steps forward and one step back historically speaking. If you have time on your side the markets are hard to beat for passive use of your money.

KHNC I think we can agree the investing in anything better than putting with that outfitter in ID that got you ;)

I’m down, but buying huge chunks in certain sectors. Patience. If you’re still fairly young, wait it out. A lot of bargains out there and the bounce back up will reward many. Not for the faint at heart.

Time in the market beats timing the market.

To correctly invest in equities for retirement, you should scarcely notice variations over 2 or 3 years, let alone a couple of weeks. I only need to know my 30-year rate of return.

"KHNC I think we can agree the investing in anything better than putting with that outfitter in ID that got you ;)"

Montana, LOL.

I still have safe investments in my actual 401K. Not everyone uses the stock market for long term. Some use it for a short time, and others have to get out at some point. Cant always just wait and wait and wait. I chose to use real estate in this case. Sounds like yall have a plan. Of course, dont ever take dale06 advice. That guy is always quick to piss on someone.

Along the lines of what JohnMC said, a wise man once said, "it's about time in the market, not timing the market." The average historical annual gain of the S&P 500 index is around 10%. At that rate, a $10K investment 30 years ago would be worth $174K today. If you worry about one month, or even a year, stocks probably aren't for you.

Matt

The drop in March 2020 was significantly more than this correction and I didn't sell then why would I sell now. What does worry me is that we have two incompetent people in the Whitehouse and a Treasury Secretary that is a political pawn. If they started listening to Lawrence Summers a prior Democrat Treasury Secretary we wouldn't be in half this mess. The reluctance to change course one tiny bit is what scares me the most.

^^^ this. I also own three properties in CO, and even in one of the hottest real estate markets in the country, my valuations haven't come close matching the stock market over the past 25 years, percentage wise, when you factor in property taxes, maintenance, etc..

Just to clarify, my retirement account is very diversified and more conservative. I really don’t touch that one at all and just let time take care of itself. I have a separate brokerage account 100% in the stock market and I’m very aggressive in it. This is what that looks like….lol

Since I am staring at an early retirement decision, yeah, January has me nervous, but I have until late 2023 until I touch any of that money. AT least that far out, so the logical part of me says, no worries, that's 2 years. The nervous part of me is watching close before I make a final decision

Rocky when you reach retirement or nearing retirement that is the time you have to change things up. Certainly should not have the same approach in or near retirement you did when you were 10 year plus from retirement. No doubt navigating through retirement investing has been tough with with the low interest rates we have seen for many years. Low interest rate are great for businesses, those they are buying homes, or anyone that needs to borrow money. It also been good for the markets as many have put money there since nothing else (bonds, CDs for example don't pay anything). It is tough for those trying to earn income off their money and almost forces you to take more risk than in the past during retirement.

These are reason I think it important to have a good competent financial advisor you trust if you are not savvy to what your options are and/or tend to make emotional decisions when things are bumpy. Especially as you near retirement. If for no other reason than to give you a idea of how much money you can spend and likely not run out of money before you die. If you have no clue to that question and there is really no precise answer. However you should be able to get within the ballpark you should quit spending until you do. You would hate to get to say 75 and realize your almost broke.

Speaking of stocks, that was a nice rally into close, today!!

The current wisdom is when retiring put most of your money in "safe investments" but if those safe investments have such poor returns then why not keep invested in stocks and have a year's worth of cash. Even if you have a few years worth of losses the overall gains of the balance of your funds in the stock market will probably surpass those losses unless we run into a five year bear market.

I would advise anyone to get in and stay in. Don't let the ups and downs worry you. The stock market IS the economy. It represents every sector of economic activity in our country and the world. Over the long run it ALWAYS goes up. Hang tough, compound interest is a beautiful thing.

Rocky not a smart guy but BC is correct. No don't get started by picking one stock and putting all your money there. It is certainly better to have a plan. With that said if you are a young guy or even a not so young guy pick a fund or two and start squirrelling away money, is far better than doing nothing because you don't know where or how to start. Investing is certainly intimating at first. Set a goal to save at least 15% of your income for retirement. If every 20 something out there would do that and just stick it in a index fund that follows the S&P and nothing else (am I not saying that is the best plan) they could not help but being wealthy by the time they reach retirement. That money is for retirement and nothing else. You are not going to touch it for vacations (even if that vacation is a hunt), emergencies, a home down payment or anything else. Before you do that make sure you got at least 6 months of money in cash in the bank that way when things come up and they always do you don't need to reach into retirement funds. If you are saving for a truck, vacation, down payment on a house have separate accounts for that. If those are short term goals keep it out the markets. Last thing look at a amortization calculator where you can see if you put in the same amount of money each year with a assumed rate of return where you will be in 10 years, 20 years, your target retirement date. Because when you can see long term effects of your savings it makes it a lot easier to squirrel that money away and shoot your current bow for another year instead of spending on this year new bow.

Bottom line doing something is better than nothing. Down the line you can get a little more sophisticated.

We “got in” the stock market and other investments about 35 years ago. Wife and I use an investment manager. It was the most important financial decision We’ve ever made. He found lots of investment opportunities that we would never have found. And he helped us adjust and re balance as needed. I have no idea what he makes off our account, but I know what we’ve made. And I’m ecstatic with the results.

Just remember you haven’t taken a lose until you sell! Investing should be a long term plan, not a short term gamble. If you want to gamble go to Vegas. Or take some amount of money you can afford to loose and invest it in aggressive ways. But the best way to build wealth comfortably is dollar cost averaging over time with making adjustments as fiscal climates change. With the current person guiding this country hand on!

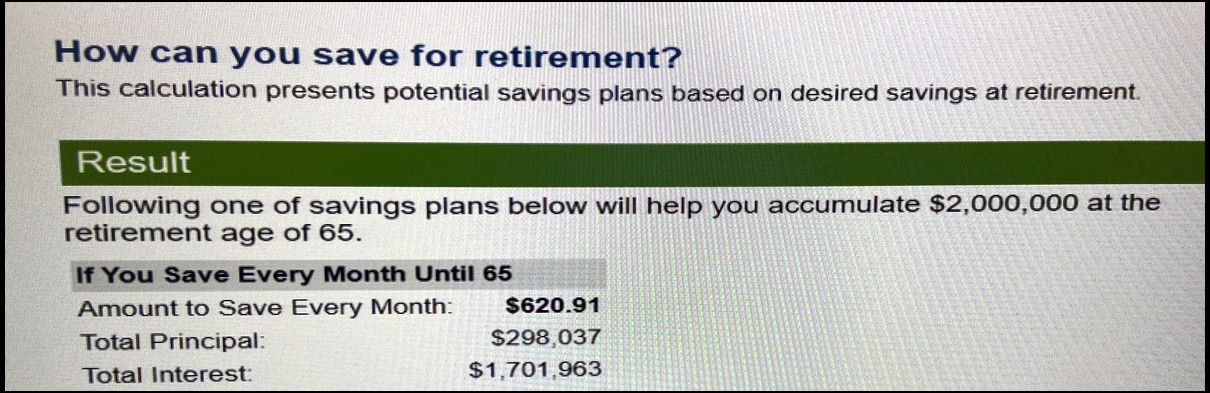

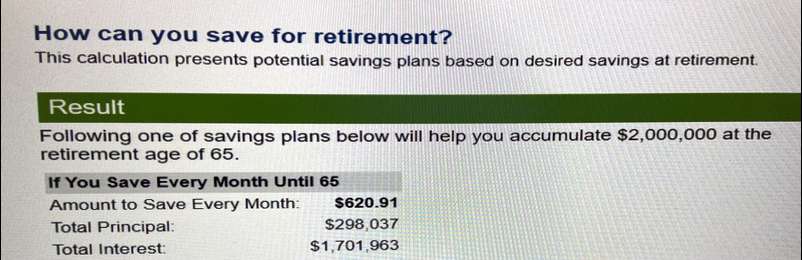

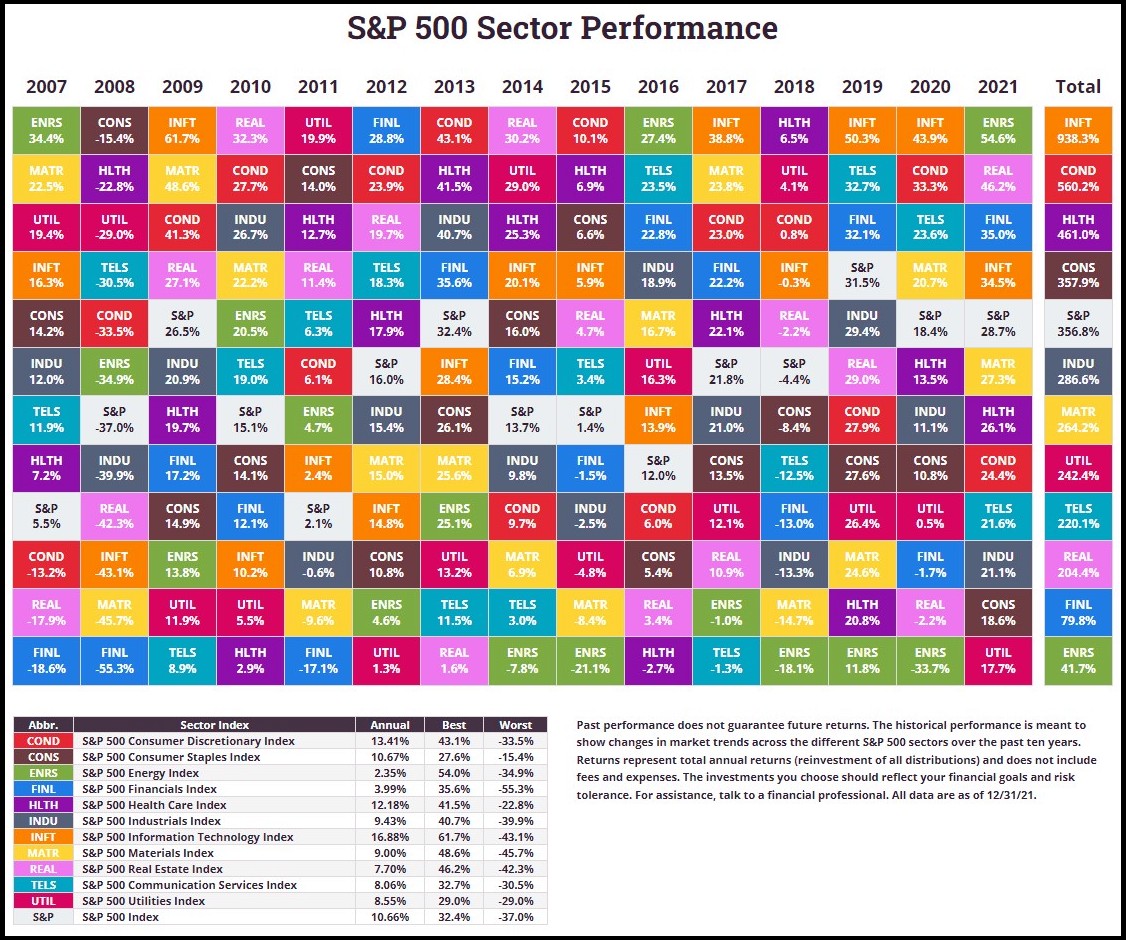

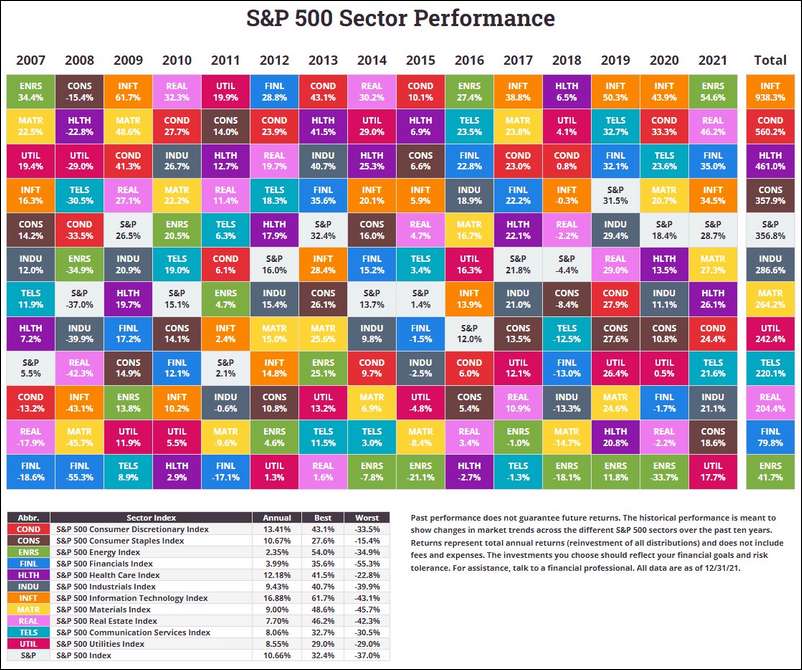

Forgive the screen shot of my computer screen. But what this picture shows if you were 25 years old saved $620 for 40 year or until you are 65 you will have 2 million dollars at retirement. That is doable for many! If not $310 a month still a millionaire at retirement. That is assuming a 8% return.

The concept of relying on an investment manager kinda makes my skin crawl. No one will care more about your investments than you. I realize it takes some research and study, and some people don't have that time. But, financial literacy is as important as learning to read and write, IMO. It's not "rocket surgery" as my friend likes to say.

Rocky, as you know, investing is a balancing act between risks and the time frame you have before you rely on your investments. I maintained an aggressive investment strategy while my wife and I were still earning at our peak. Now that we've both retired, I've adopted a conservation over growth strategy. About 1/2 of our net worth is in debt-free real-estate. The rest is about an even split between stock, bonds, and money markets. The net annual gains of our investments more than pays for our cost of living, barring any unexpected financial disasters, like serious health issues or some natural disaster.

Matt

I partially disagree with Matt but for some it can work. What he said is kind of like saying nothing is more important than your health so I am not going to trust a doctor with it. This thread was started and not picking on KHNC by someone that was letting emotions choose what to do instead of logic. That is easy to happen even for a guy like me that likes to think he has no emotions.

I agree is not 'rocket surgery' when you are just socking away money. I think as you start getting closer to retirement and into retirement you better be very financial literate if you go it alone. If you use a advisor pick him or her wisely. Some are really good other not so much and some are just easier to relate to and understand.

Rocky, I never doubted you know how to properly invest for retirement. It's not the black magic some think it is.

Matt

I'm not looking at it. I look at my money once per year.

I did just sell a house and have a bunch of cash that I'm not sure what to do with now.

Ike….Maybe a Stone sheep hunt?? You’re not getting any younger!

I sold some stuff going to 35% in cash at the beginning of the year with the intent to sell more…but didn’t. Im overweight energy (ETFs) and high dividend stocks like TRTN and KMI.

I had some huge gain in a few ETFs that I have owned for years. I found myself evaluating whether it was worth it to sell it and pay 50% in taxes on the gains or just ride it out. A couple of those are down 20%… it remains to see whether I was right.

I think the 7% reported inflation is way under the actual. The current government policies will only exacerbate inflation.

I’m looking to buy the semi index SMH, MGM, CSR, and a few others but I’m waiting for a sign of capitulation.

I’m always looking for a trade and open to ideas, hint, hint. Grin

All I can say is this....If I had the IRA Opportunities in my 20's I would have easily retired before 50 instead of 58..... There is always money to be made in any market.... For those of you who get hung up on politics and listen to the BS from both sides, yeah, you lose its that simple..... At 72 I readjust,,, of course I have taken losses, only to have more opportunities in the future, like today......

The trick is no debt, except property, which I have just bought more,,,, As far as a vehicle, would not waste my money, but will buy land,,,,,,, 'some of you should wake up, because there is alot of opportunity out there,,,just open your eyes

JohnMC, it’s interesting you posted that screenshot showing what saving X amount can do.

After graduating college, 1991....I had an extra $10,000 or so. My local banker encouraged/begged me to open an IRA and just make the max contributions per year. She told me that...”I’d be swimming in money” at age 65. I’m now 53 and think about that missed boat all the time!!

At 22 years old, my mind was on other things. I couldn’t comprehend 45 years in the future.

To the risk adverse,one of life’s most expensive hobby’s is checking your portfolio Chasing returns is a losing proposition for most.I’m a mutual fund investor,buy and hold and realize markets go up and markets go down and avoid the noise.

For ME,that presently has been working for 30 years

Fees and trying to time the market are perhaps the two largest inhibitors to maximum returns. It’s hard to beat a low cost strategy made up of long term investing at regular time intervals in market index funds. I’ll take that every day of the century over someone charging me for their “expertise” in addition to using that “advice” to time when I do or don’t invest. The math proves it.

Agree with Genesis & Mqqse.

And I'm not that interested in gradually moving more and more capital into "safer" funds, as I approach retirement age. What for? It's not like I'm waiting for retirement day to then spend all that money in one chunk. The reason for saving is so that we can later withdraw a tiny percentage (say 2-4 %) annually to live on, if needed. The bulk stays invested, so why would I want to accept lower returns, ever? If it's only so that I won't have to worry & fret over every market swing, that's a fundamental mistake.

I'll retire (probably) in about a year and a half whether the market is up or down. Agree with Genesis and my investment risk doesn't change the closer I get. I have 2 investment advisors I trust.

Mqqse, glad that apparently worked out for you. Me hiring an investment manager in the early 90s made us money far beyond any thing we could have done alone. He is into this stuff 60 hours or more per week. We were in careers and had little time or expertise to find investment strategy’s. As I stated above, I really don’t know, or care what he makes off our account, as long as our investments do well. And they have done exceptionally well. It’s “net” thing for us.

Sticksender,

The reason to move money into less risky investments near retirement is to conserve the gains. A retiree typically doesn't have the time to recover from a major market crash. Remember, a 50% crash requires a 100% gain to get back to even. I know several retirees who were crushed by the 2008 financial market crash because they weren't hedged against it. All of them had to drastically scale back their lifestyles and costs of living. A few even had to go back to work.

Matt

According to our 1099s coming in & capitol gains we did pretty friggin good. Wife draws from hers & recovered all her distributions + gained. A few years ago I said to the wife, Market went over 17 so were makin good money. Ummm, Double + since then.. That being said our financial advisor is "excellent" & is in contact on a regular basis & we feel lucky in that way.

“Of course, dont ever take dale06 advice.”

In this case, he is spot on.

X2 on dale06!

Those of you who think you can time this beast are only kidding yourselves. You may get it right a time or two, maybe enough to build some dangerous and imaginary self confidence. Then with that false confidence you’ll make bigger bets, only to get it even more wrong eventually, hopefully without catastrophic consequences. Then ultimately, you claim that the “system” is broken because it didn’t go your way. I hope you traders aren’t doing this with money you’ll eventually need.

Those that maintain a long term view that ignores the noise are doing it right.

The "fear of loss" in retirement investing can be a self-fulfilling prophecy. Investing too conservatively over decades of time means you build less, which in turn reduces your ability to tolerate loss.

How are yall that were such huge proponents when i mentioned this 5-6 weeks ago?

The bulk of my money tied up in the market is in retirement accounts that I likely won’t touch for 15-20 years. So these corrections we’re seeing now mean essentially nothing - if anything, it gives me a bit more buying power at the moment.

Like we talked about, if you are in a position where you cannot tolerate a 5-10% correction (or more), then perhaps the stock market isn’t the place to keep your money.

MQQSE is spot on.But any kind of investing is better than nothing,even if you use the (guy).

+1 Dale and GG. No one foresaw the crashes in 87, 2000, or 2008. But someone invested in an aggressive portfolio and retiring in those years, drawing from their portfolios for living expenses, will not make that up for decades. Maybe ever. Their carefully calculated withdrawal plan could result in much lower standard of living in retirement.

I switched to a professional (from mostly DIY) a few years before retirement, when I had "enough" money. I'm not greedy, so we went more conservative and moved some more into a solid annuity I was building. Yes, I lost out on some gains, but no one can predict the future and I couldn't risk another 2008 with my short window. I'm not sorry. My advisor is a bowhunter I've known for a long time and I trust him.

Now retired for almost 8 years and remarried to someone with a good gubmint pension and her own fat investment account. We are living confortably on my annuity, dividends, SS, and her pension, and our investments are just play money. Our income is not affected by market swings. So we moved a bunch into more aggressive investments. But if I was drawing that formulaic 4-5% a year (pick your number), I would still be in a very conservative portfolio to minimize the risk.

For guys reading this that are new or just thinking about getting into investing. Some the debates above are not that important and just makes this topic seem harder than it needs to be. It is lot like which broadhead. You could say using an advisor is a mechanical broadhead and and not is a fixed head. They both work but you need to do one or the other. I can think back to when I was early 20's I had some cash sitting in checking account it seemed like a lot at the time. I happened to meet a Financial advisor he invested that money and more importantly got me investing some out of each paycheck. First max what your company will match in a 401k, what they match is free money. Then max what you can contribute to it (it is pre-tax). That is easy. Your company will have a list of funds to pick from if not sure as a trusted co worker. Get started as your nest egg grows you can get a little sophisticated in what funds and types of accounts. The most important part is you are putting away money for retirement. Remember 10k when your 25 is the same investing about 40k when you are 45 or 160k when you are 65. Started today don't wait. It was one the best decisions I ever made.

"Risk Adverse" to me only applies to not being emotional at one's present asset allocation.I fully expect I will move my allocation from less stocks to more bonds as my time from retirement decreases. Some individuals can stomach the ebbs and flow of market volatility others can't.Some investors need an advisor and others do not to meet objectives. Inflation is presently a small rock in my boot though.

Best investments I’ve made to date were in real estate but not because I had a pile of cash to squirrel away somewhere. Paying cash for real estate vs buying into market is a tough call. If you don’t have much to begin with, my comparisons seem to show rental properties blowing stocks out of the water. Throwing 20% down on a rental and allowing it to pay itself off in 15 years from there coupled with the equity gains along the way nets more than a mutual fund with the same timeline.

But I am young and finally had some good advice stick. Never think you know it all and have an egg in as many baskets as possible. I use play money in day trading to learn more about the market. I aim to pick up a new rental property every 1-2 years, and utilize a money manager for my other market investments, they know more than me and I’m okay with admitting that!

You can go on many investment sites and take a short 'test' to determine how much risk you are 'comfortable' with. They'll usually cook up a mix of funds that matches your 'profile.'

Or just invest in a 'target date' fund, which automatically tapers your investment risk downward as you approach retirement age. I did that several years before retirement with my IRA. My 401-k from my last job is still a moderately aggressive mix. Neither is immune to nor overly sensitive to market fluctuations in the longer run. (They did drop some this month, but I'm still well ahead of where I thought I'd be several years ago.)

I do some market timing in the context of managing risk.

If you don’t think we are going into volatile times with this president you have your head in the sand. A week president creates big problems. Trump was a bully and an ass, but he was our bully. ( Some abhor politics- sorry but politics matter)

There are many negatives out there inc the Fed raising rates which is historically bad, Massive inflation, Russia and the big dice roll: China/Taiwan. What if Biden keels and Kamala takes over? I’m OK with keeping a little over a third of my stock mkt money in cash.

Whether the market goes up or down in that time- I can’t read the future but it doesn’t look good. I’m content with keeping a percentage of my money in cash to manage the risk.

An investor always has to consider the tax consequences not only on sells but also buy strategies. I treat trades differently than I treat long-term investments using trades to offset gains and losses in my taxable accounts- multiple accts to get around the 30 day rule… and trading in my Non tax IRA.

I am a big proponent of the reversion to the mean theory and it has made me a lot of money over the years. Charts are very important and tell you a lot. Take a look at the chart of Nvidia or Moderna and that’s all you need to know. I do not buy stocks on a steep ramp ups, and will capture profit a steep run up, they always come back to earth. I always try to buy down around the 50 day or the 200 day MA mostly dollar cost averaging in. I don’t try to capture every dollar on trades and I try to stop out losses though that doesnt always work.

I stay away from companies that have zero earnings. Yes I have missed out on some big gainers but it’s part of my managing the risk strategy, I’ve also saved myself from some big duds. For every Tesla there is a Lordstown..

I look at forward trends….industries (ETFs) that I think will do well. I dont care much about past performance. A guy buying the Software index 30%+ off its highs will probably see a little more pain in the short term but in a few years he will way outperform the market. I question; What will do well in the next 5 years…. And is it a relative value is the way I approach it.

I sometimes capture gains and offset risk with covered options.

High flyers like Tesla will need 100 years to catch up to its stock valuation. Too much risk there for me.

The key to being a good investor is to have a strategy and to stick to it, take the emotion out of investing. I think a young guy would do well to study those topics above and develop his own strategy.

.

Investing in real estate can be as foolish as investing in stocks.

Chose poorly with either one, and your money will get better use buying slurpee's and hot dogs at the local 7-Eleven

I’ve done very well and I consider myself very lucky. I do all my own and have been way ahead of the market averages for a lot of years. I also have done well in my real estate holdings I have never lost a dime on any property that I have sold. I was lucky when I picked up a lot of Apple stock and it has done very well. I regret selling my Home Depot and Crocs while they made a nice profit they’re a couple hundred percent up from I sold them for. I always chuckle at my saying pigs get fat and hogs get slaughtered if that makes sense.Good luck Lewis

One very important thing to keep an eye on with any investment is what kind of fees you are paying. Too high fees will cost you tens of thousands of dollars over time. Insurance companies, that often sell annuities, are notorious for baking in fees that you aren’t even aware of if you aren’t paying attention.

Lewis,

Almost 20 years ago I got interested in trading stocks. Back then, brokers required you to fill out a lengthy application, including bank and tax statements. They all had a minimum deposit requirement, and they charged fees for every trade. IIRC, it took 3-4 weeks for my account to be approved. I started with an amount that wouldn't kill me, if I lost it all.

I began enthusiastically making numerous trades per day, while chasing a few percentage points with each trade. I soon learned I was spending more on trading fees than I was making in returns. The one stock that I let ride during that period was Apple. Holy cash cow!! It taught me the value of buying quality stocks and holding onto them. So, I added Amazon and Intuitive Surgical to my Apple shares, and let those 3 positions ride ever since. That small account has paid for 2 new trucks, a boat, and numerous vacations, and is still worth over 3 times what I invested. I often dream about what our retirement accounts would look like if I'd invested everything in just those 3 companies. 20/20 hindsight, of course.

Matt

G G you are correct picking quality stocks is really hard to argue against I every now and then gamble on an iffy stock some have done well others not so good. I also like to carry some high paying dividend paying stocks I have a couple that have averaged around 12-14% over the years. I got hurt a little on those when the pandemic hit but they still paid their dividends so I can’t complain.Good luck Lewis

If you ever wanted to own a titty bar you can buy RICK. I just looked it up I owned a little of it several years ago made a little not a lot but just looked damn thing quadrupled during COVID. No one told me lap dances prevented the China Virus.

This is one of the better threads in awhile. Lots of sound advice here. Pros are much better than me and are a great option so is diy - kind of like hunting. . Been doing my own for a long time so do my own thing. Can go stocks, funds, index, managed. The best time is when you have the sooner the better. Lots of advantages Esp in 401k where there is a match as John said. Plus Retirement accounts enjoy tax benefits ( now or later). Warren Buffet and Charlie are still killing it because they apply so much common sense and invest in what they know/ understand Love what slot of you guys are doing. Ps - I saw a derogatory post directed at Dale - he has NEVER had a bad post - imo

Buy the S&P 500 index and add regularly. Never look back.

Steve b is on point but I also do VT and VIG to reduce my exposure to overvalued tech.

Am I down this month, yes. Am I up a LOT in the last 6 YES.

I'm beating the FJB inflation so I'm good.

Be sure you understand the mechanics of a cap weighted index if you are going to blindly throw money at such funds. I’m not anti index fund at all, I use them too (in etf form), but in a unique way. Cap weighted indices have created concentrations and additional risk that most individual investors do not realize. Do some research and make sure you understand this subject and are aware of the increased risk. The consequences otherwise might be surprising.

Sticksender

The reason to move to conservative investments near retirement is a simple reason.

Once you won the game you quit playing.

If you won the lottery, you wouldn’t really be out there spending all the money on lottery tickets and gambling more at the casino to win again. A smart person would realize he just got lucky, now it’s about preservation.

You can draw parallels between investing and archery - some guys like to 'keep it simple' - buy a bow and arrows, have the local pro shop keep them tuned and shooting. Others like to tinker with bows, build arrows, do as much of their own hands-on as possible.

Investing can be as simple or complex as your interest dictates. Pick your own investments or go with a broker who understands your needs.

Personally I'd rather spend time shooting than watching the market. ymmv

I have been in over 40 years, it has gone very, very well.

sasquatch, my question "what for?" was actually just rhetorical. I do indeed already know the reason guys think they need to exit higher-yielding funds as they approach retirement. They believe this "preserves their wins". My approach is the opposite, because for my own purposes, with regard to that segment of my savings, that concept is faulty for my way of thinking, and guarantees long-term loss. It doesn't make sense for me, so I'll stay invested in stuff that has proven over the long haul to yield the best. In retirement, I want my yield to draw-off ratio to be as high as possible. That means I won't back off high-risk, high-yield funds, nor try to out-guess market timing. Like most people, I won't be taking it with me. Might as well leave the heirs in the best shape possible. YMMV, so do what's best for your own peace of mind.

Lots of investment advice here is spot on. The interesting thing is that everyone mentions "if only they had started when they were 25." I think that is because when you are 40 or 50 years old it is quite conceivable to save $500/month. When you are 25, not so much. Not when you are in the investment phase of your life as far as a career goes. Money is tight, you're building a family, and oh let's not forget all the other Bowsite advice saying "DO IT WHEN YOU'RE YOUNG!" ;)

I think another major aspect that comes into play for the entrepreneurial types is forgetting about the stock market, forgetting about real estate, and betting on yourself. It's a different world, and it's not for everyone. But if you can become a business owner, or shareholder and influence the growth of said business your returns can far exceed even a good stock market portfolio. In the risk/reward relationship this is by far the riskiest, with the highest potential level of return. You don't necessarily need to be a business start-up type person either. If you are an incredibly valued employee, and you know your worth it is not out of line to talk to your employer and ask about share options. If you believe in your place of business, and like where it is going, maybe you can forego some salary or bonuses in place of some shares. It can be a win-win as the employer more than likely locks down commitment of a key employee. If nothing else, it's another form of diversification. When it comes to investing in real estate, it's fun to buy hunting land, but if you're actually using it for investing purposes it had better be income generating real estate ie: housing or commercial etc.

Lots of interesting advice above. I turn 71 this week. Started an investment account in my mid 30s. Didn’t have a lot to save but did so monthly and all of the bonuses I made over the years we’re invested. I’ll say it one more time, start as early as possible, $200 a month when you are 30 is way better than $500 a month when you are 50. Time and compounded earnings are huge. I retired at 61 and have not adjusted to a very conservative portfolio. Most of us need to plan to live 20 plus years after retiring, so retiring and immediately going conservative could leave you financially strapped near the end of your life.

I retired last year at 51 and my investment manager suggested that, with the combination of poor bond yields/inflation, tax consequences, and my relatively early retirement, it would be a mistake to pursue the traditional wisdom of shifting from equities into a more bond-heavy portfolio mix.

Dale06 I started at 26 not because I thought about it but because my company gave me 6% match.Sounded like a good deal to me.When I was around mid 30's I started investing in Vanguard.I ended up retired at 51,still can't beleave how it worked out.I am 67 now and glad I did what i did.

" A smart person would realize he just got lucky, now it’s about preservation."

Dang, I must be dumb as hell... :^)

Right wrong or indifferent, my plan is to leave the bulk of retirements funds invested in stocks after retirement. Opened two Roth IRAs a few years ago and have been maxing those out ever since. Will likely go somewhat conservative on those smaller accounts at retirement. Plan to use them as income on years the stock market is down...with smaller withdrawals needed due to zero tax liability.

Based on account history, no reason to believe this is a bad decision. I can only review history online back to 2006, but during that 16 year span, accounts have only been in the red four times (12X in the black)...never red two years back to back (red once every 3-4 years)...and the worst crash in late 2008 was back in the black by mid-2010. Average gain during that 16 year span is over 12% annually. Think I'll take my chances....

I am nearing retirement. Plan on going in October of 2023. I am not really getting that much less risky. I will have a pension when I retire, and will draw SS a little over a year after I retire. This will replace the majority of my current income. I also have a 457, about 1/3 of it is in cash which is the bucket I will draw from if I need it. The remaining 2/3 is in stock mutual funds that I plan on leaving there and possibly even moving some of my cash back in there. Also my wife will continue to work for 3-5 more years. She will also have a pension to draw from, a 403b and SS. We should be good and able to still carry some risk for growth.

If I were to go back in time and start over, I would not diversify. I'd start young in S&P Index funds and aggressive growth funds, small through blue chips, and keep dollar cost averaging into them. I wouldn't have bonds at all until quite a bit later. Not even sure I'd look at International. When I researched Int'l stock funds, they rarely beat U.S. Equity funds.

Hopefully the ones who don’t believe in preserving the wealth have about 2x what they will really need.

In that sense, go for it, it would make decent sense to stay risky.

For the ones who retire with about what it will take, a 2008 crash can cripple their retirement.

It may have recovered in a few years, but for one that’s not guaranteed as anyone would agree, also it’s harder to recover when you lose 40% PLUS are withdrawing every year.

Recovering is a lot easier when you don’t have to also withdraw the money to live on at the same times it’s down.

I think that sasquatch makes a number of good points in his last comment. If we are not in a good position to ride out a year or so of a falling market, there is more risk in being heavy in equalities. However, during a time of high inflation and low interest rates cash and bonds are going to result in loosing buying power and quality of life. IMO equalities have the lowest risk over a 3+ year time frame because history has proven that they provide the best return and stay ahead of inflation. I also think that no one can time the market and that it is best to invest in long term stocks and always be in the market. If an individual is under too much stress with the short-term variability of stocks it may sense for them to be in something more stable over the short term. I have a friend whose wife wants to be involved in managing their investments, but it is agonizing for her to pick stocks and she cannot sleep at night for worrying about them. For his wife's health, he has to look for an investing strategy that appears to be safer than buying and managing individual stocks. That is the best solution for them even though it may not be the best financially. IMO some of the comments above are about what is best for the commenter rather than what is best financially which is fine as long as everyone recognizes the distinction.

Goyt, suggest your friend do what I did years ago. My late wife had a math brain. Our investments were with an advisor, but I gave her a few thousand in "play money" and told her to go for it. She subscribed to Motley Fool and a couple other DIY services, started picking some stocks, and consistently beat the market, while learning it. She would take the principal out after big gains and reinvest that elsewhere.

After awhile her portfolio got big enough that she was a little spooked, so we put most of it into our advisor account, and she kept on, except on a smaller scale. Then after she got sick, we rolled the rest over and took the burden off. But it was a great learning experience for her, and since she no longer worked outside the house, it gave her a productive feeling of contributing to our finances.

Jaquoma, I am happy that it worked out for you and your wife. It is a great idea. However, there is no way that I am going to give my friend martial advise.

I agree with the guys above.

Some of the conventional portfolio advice of more bonds as you get older fails miserably in the interest rate environment we are going into now.

This is where I recommend looking forward. Using Past returns can fail you miserably and heres why; We are coming from an extended period of artificially low interest rates. We have had the Lowest home mortgage rates in my lifetime (6 decades) These can be manipulated for awhile…but not forever.

It doesn’t take much investment knowledge to see this upcoming trend.

The challenge with predicting what stock investments will work in the future is 2 fold. 1) what industries will work 2) what is their relative value

Tesla will sell more cars for sure…but at their $935B valuation, and only a tiny % of profit, the PE of 190 tells you it will be 190 year payback at the current earnings. Sure they are plowing $$ back into the co and no doubt their eps will rise….the Q is will it rise exponentially in the future now that they have a lot of competition? Typically when companies my first market they rock it up but as competitors come in their margins go down.

Do you think the need for semiconductors will rise in the coming years? Its an absolute certainty. Dollar cost avg into SMH will be a double in the next 5 yrs, the one negative would be if China takes over Taiwan and TSM.

One other thing to consider is that, during the wealth-building phase, it is typical to reinvest dividends/distributions. When one retires, it may be better to have those remain in cash. Simple stuff, but better to only pay taxes on the dividends/distributions than that plus cap gains on sales of stock if they get reinvested.

I was pleasantly surprised when I thought I was going to have to sell securities on 1/2/22 to fund our 1H22 household expenses to learn that Plus a bit more already sitting in my investment account.

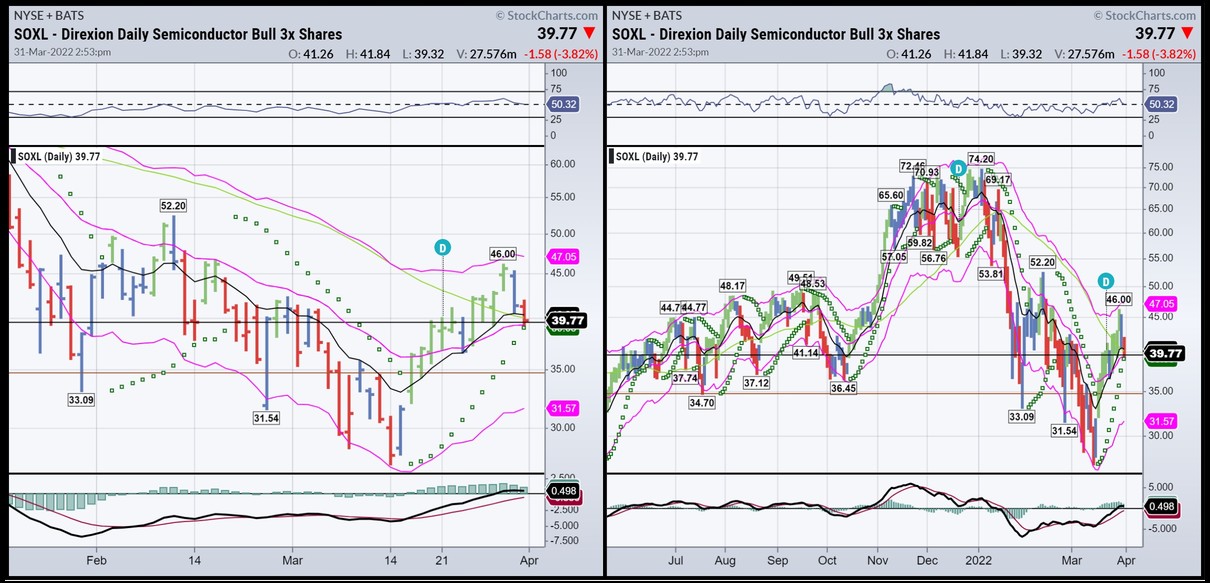

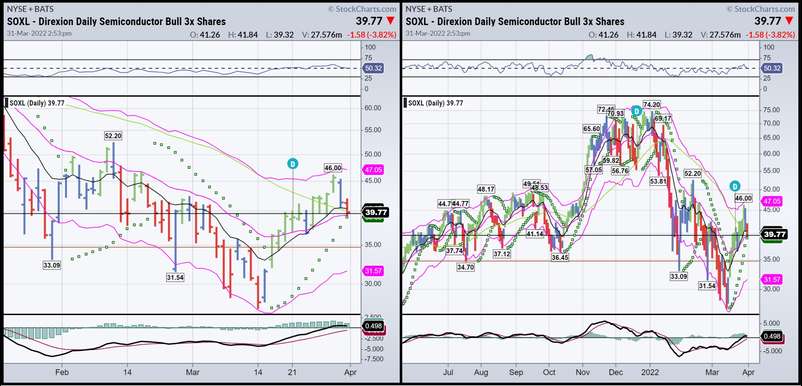

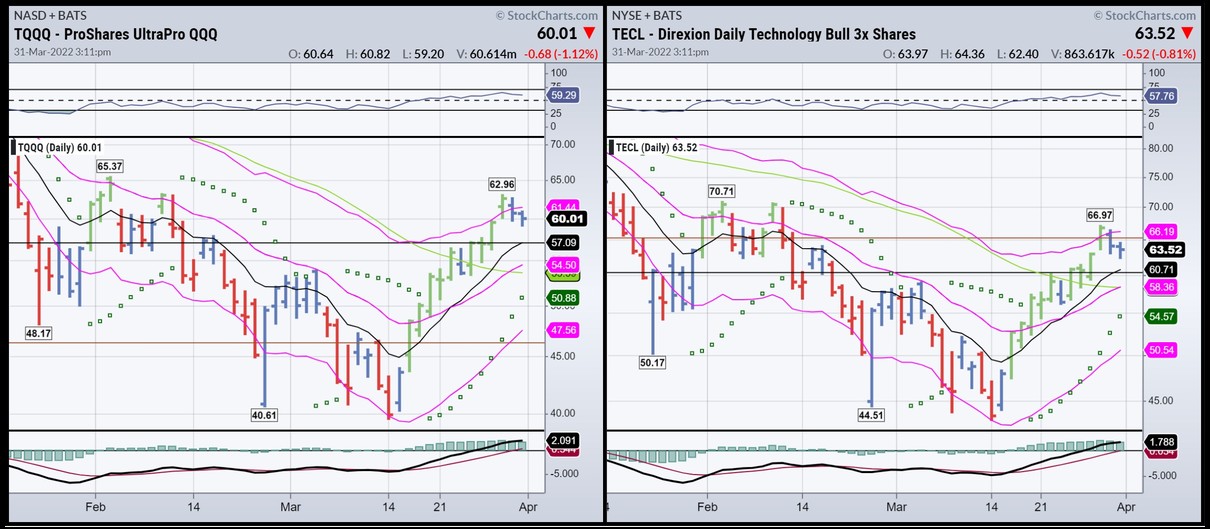

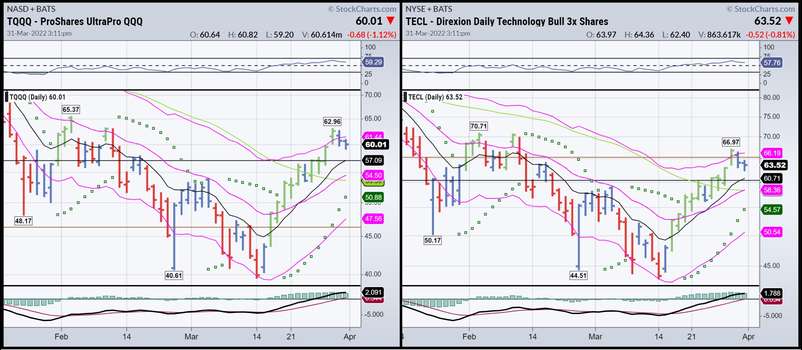

So is this a dead cat bounce?

Matt, I agree with you on the dividends. They are taxable in the year received regardless if they are reinvested. By getting cash, the option to buy any stock or use them for expenses is there. With free trades the attractiveness of reinvesting dividends is not as great. Once the dividends are reinvested it is not possible to sell stock to get their value out of the market w/o incurring capital gains in most cases. I look at dividends almost like social security as a guaranteed cash flow. Some stocks may drop dividends while others increase dividends is the short term and in the long run they go up.

My Crypto currency has tanked. I may jump off a virtual building :>))))

As always the level of experience and expertise among the regular Bowsiters on various subjects is outstanding including this one. Hopefully the young here will take the time to digest what is being said here and make some good financial decisions. I think that this thread could be a good basis for a high school or college course.

Personally I hope all crypto currency goes to zero. A false market. And a drug dealers dream.

sticksender, FYI, while I understood what you meant, you are using the term "yield" in the place of total return. By definition, there is a difference. Yield is exclusively income generated by interest and dividends. Total return, on the other hand, includes yield, but also adds or subtracts the appreciation/depreciation of the investment's value. In today's environment, if you were to depend solely on yield, you might be in trouble!

Those of you guessing your proper asset allocation based on age, or winging it based on what feels right, or historical returns, or current market conditions, anything else, you need not do so. As is the case with most things related to investing, with a good financial plan, you eliminate the guesswork. A plan will detail and quantify exactly how much you should have in specific asset classes to meet your unique goals. Let the math decide. Not emotions.

I am feeling pretty good. I'm 55, retired for almost a year and have approximately 40% of my non-real estate investments in Bond and Income. I have never believed in timing the market. Put it in and keep it in. I believe it is well proven that you will not win the timing game vs consistent investing of surplus funds. I shifted from 70/30 to 60/40 a year ago. Additionally, 1/3 of my non "liquid" /non 401K/IRA investments are also in commercial real estate holdings. My goal with equities and bonds was to yield at least 4% per year once we retired (ya, the 4% rule) and we have been fortunate to soar past that during the last twelve months. I fully expect a 30% correction when it all hits the fan. Will be a good time to pour some more cash into the market, or even better maybe pick off some real estate at a reasonable price.

4% per year (without liquidating assets) used to be a no brainer for our parents and grandparents. But these days with near zero interest rates, it is a challenge. It requires everyone to take more risk, relying on greater concentrations in stocks. You have to supplement your bond and income producing assets with appreciation in the stock market. Not the ideal situation, but necessary today. Fortunately, everyone is chasing the stock market, placing excess cash in there. This is helping to really drive the market. Will it have a hard correction? You bet, but I can guarantee you before long everybody will be all in again. Add to that the government will eventually have turn on the quantitative easing again. That is just more capital that will get dumped into the markets, driven prices up further.

Don't forget, it ain't a gain or a loss unless you sell it. Unrealized does not count! Best advice I can give is don't look :)

peterk, don’t look is great advice! I only look when the market hits a new high. This past year was unbelievable given the political mess we’ve been in.

Since you brought up the “4% rule”, I wonder what some of you more experienced guys think about that. That has been my plan when I retire in 8 years at 55 (my plan anyway). I’ve been reading some stuff that says to maybe dial that back to 3.5 or even 3%. Also, anyone have any knowledge on the “rule of 55” for accessing your 401k at 55?

Deerhunter72, The 4% is just a rough rule of thumb, very rough. It may work for some and not at all for others. As I have previously said many times, why rely on any rule of thumb? You are a unique individual, with assets and goals and preferences that are specifically your own. You don’t need this or any other financial rule of thumb. Instead, devise a quality financial plan and it will tell you precisely what your withdrawal amount should be. With statistical analysis, this number can be nailed down to the dollar, with 90%+ accuracy. Again, there is no need to guess at this. There are basic plans available online. And of course comprehensive plans can be produced by a fee only professional who is held to a fiduciary standard. Get the answers you deserve. Best of luck to you.

Deerhunter72, my income/ bond investments returned 2.8% last year. Blend that with modest growth in the equity portfolio, and your there. Some years you won't hit it, other years you will blow it out of the water, like last year. With interest rates increasing, the bond side of the market should see better yields this year.

Higher yields, potentially, but also greater likelihood of principal loss. There is an inverse relationship between interest rates and the prices of bonds. That’s not conjecture, it’s mathematics. Use caution.

SDHNTR, thanks for the response, I value your opinion as a professional. We do work with a fee only advisor and we have a plan. He would like me to work longer, only to accumulate more money, but agrees that we can both retire at 55 with a safe draw down that won’t leave us penniless. I asked about the 4% rule because it’s a big topic with the FIRE community. I sometimes listen to some their blogs and find it interesting.

Peterk, thanks for responding. Sounds like your plan is working well for you.

I was fortunate someone pointed me in the direction of Vanguard in my late 20s and read Jack Bogle's Common Sense on Mutual Funds around the same time.

I also found the Trinity Study around that same time from where the 4% Rule originated which has impacted my decision making.

Attached is an article on the study somey may find helpful.

Take care. Mike

I am up about 6% this year. I have 25% shorting the market, 25% in stocks with dividends of at least 7.5%, 25% in oil (XOM etc) and 25% in cash waiting for the crash I think is coming in a year at the most. I actually sold 5 rentals last year to free up cash to invest into the market when it crashes.

I predict real estate will be down about 20% by the end of next year and I plan to buy some more rentals.

Vanguard has a very good page on there web sight called how long will your money last.Its like a video game.

something to consider is the rate of inflation. I see that it was 7.1% for 2021, so, I believe I have to outgain the inflation rate every year, or, I've lost money. For 2022 if we have high inflation and low returns it may be a negative year? Time will tell.

Everyone is stuck on inflation this year, which I understand. I am too

However we basically had 0 inflation for a long time previously. Overall we are way ahead as most were still getting raises all those years on top of investment growth.

Jaq brought it up…and I would agree that investing is not rocket science.

With a few rules anyone can do as well if not better than the investment advisors that charge you a % of your portfolio then plug it into index funds or even worse, high commission annuities.

Aubs, thanks for the link to the Trinity Study. I've heard a lot about it but have never really read much on it. Our plan is not set up on a hard and fast 4% draw, actually a little less I think but I'd have to look at it again.

Beendare, annuities have their place I guess, but you're correct about the high commissions. Those fees can suck the life out of the rate of return and a fast talking salesman can make them sound so good. We are in the process of getting my wife out of one and they don't make it easy.

Beendare, if you hire an investment adviser or manager, and allow him/her to put you in annuities, thats on you. I’ve had an investment manager for over 30 years. I or my wife approve all transactions before they get executed. He calls us with options and recommendations and we decide whether to proceed or not. He has never suggested an annuity. I’ve said before, I do not know what he charges us. We are concerned with the “net” and it has been very good. He has access to and the time to examine many investment options that we would not see without him.

Dale, any broker calling you with "Ideas" is raking a commission, fine if he has beaten the market....VERY few do.

Not all Annuities are bad...you can buy them direct from Vanguard....just saying, beware these can be a very high commission check to your advisor as evidenced by the long lock in period. [the advisors here will back me on this if they are honest]

Many of the financial planners are essentially salespeople. NOT all.... and its worth looking for one thats not. Many just plug your money into pre determined portfolio allocations by your age group following typical portfolio designs which you can get these yourself on every online investment company if thats the route you want to take.. I have a couple buddies that have done very well doing just that.

I'm not disparaging brokers....just pointing out this is not rocket science.You can do this. A no brainer strategy if thats what you want is Dollar cost averaging into diversified funds. The stats show that this has beaten a huge % of Hedge fund and other investment advisors over the years....without the fees. Spend a little more time understanding trends and reversion to the mean........and you can do extremely well.

When you think about it, annuities are a "heads I win, tails you lose" situation for the insurance companies who offer them. They are a perfect hedge to their life insurance policies. There's a reason insurance companies are among the most profitable companies on the planet. The odds are always stacked in their favor, just like a casino.

Matt

GG, I agree 100%. I won't go so far as to say they are crooks, a business seeks to make money, but your comparison to casinos is spot on. My wife is a teacher and until recently her only option from her employer was a 403b sponsored by AXA(now Equitable). It has been better than nothing but the slimy rep lied to us repeatedly about the fee structure a few years ago. It was a waste of time, but I did file a complaint against him with FINRA.

As Suzy Orman says, "Investments and investments, and insurance is insurance, don't mix the two."

Annuities make sense for a very small percentage of investors. Yes, in my opinion, they are largely oversold. Usually on a commission basis, but there are also some fee-based iterations available now too. They are emotional investments. Some people don't care about the cost (assuming they are properly informed), they want guaranteed income and they can't stand the thought of their potential for retirement income being linked to the volatility of the stock market. I won't universally bad mouth them, but like anything else, you should know what you are buying and why you are buying it.

I wonder how many billions of investor's money wind up in the insurance company's coffers, when the investor dies before the term of the annuity contract is up. I think you'd have to live to around 135 years old to ever see your entire principal amount with most 'lifetime' annuities.

Matt

GG, that's only if you annuitize, which rarely happens with variable annuities nowadays. With more modern annuities and living benefits, you can realize income without having to annuitize and don't lose control over your principal. I'm not advocating them, I'm just stating that what you mentioned is really a thing of the past with most annuities used today.

I am one of those who did invest some money in an annuity. I knew exactly what I was getting into, did the research, and found a really good one (lifetime balance grew at 6% a year, more if the market was way up). 2008 scared the hell out of me with a relatively short timeline to retirement. I wanted a guarantee of some lifetime income to supplement SS if the market did a few more 2008 collapses, especially early in my retirement. So I rolled over what was a pension lump sum from a former company into this annuity with a much better return, added some to it, and I could draw from it anytime instead of waiting until age 70 (per the pension stipulation)

Hindsight is 20/20. That money would have appreciated more in the market over that period, but like I said, 2008 spooked me. Nobody knew what would happen, nobody knew Trump would enact the policies he did. At the time, we had Obama and the Dems in power, and I had little faith in their fiscal responsibility and the reaction from the equity markets.

So now I'm drawing from it, and coupled with my SS, not only do we live very well, but I have a couple thousand left over every month to roll back into our mutual funds. I will regain my principal in 9 years (from when I started drawing).

Yes, inflation is also a concern, but I'm not sorry I did it. Nobody knows what will happen with the market in 20 years. In 9 years when my wife draws from her SS it will more than compensate for any inflationary pressures, plus she has a Federal pension too. Her pension goes right into our portfolio now, as well.

We have three paid-off houses in a hot real estate market, a nice fat diversified investment portfolio we don't have to touch besides adding to it, and every month that annuity deposit drops in and makes me smile. Doing ok considering I was totally broke and in debt at age 40, and retired on my 60th birthday.

But I totally agree that annuities are not for everyone, and there are some scammers out there who overpromise and under deliver. Buyer beware.

Nate,

I've never understood not annuitizing an annuity. Doesn't a T-note or bond provide about the same fixed rate of return, while preserving the principle? It's been a while since I looked into annuities, and decided they weren't for me. Maybe they've changed.

Matt

GG, if I had found a T note or bond in 2009 that guaranteed 6% plus a bump (with cap) when the market overperformed, I'd have jumped on it in a second. I did invest in a commercial REIT that payed a 6.5% dividend and seemed pretty solid, but my principal has declined about 30% since COVID bashed commercial and retail, a reverse split, and the IPO.

Lou,

I've had about 25% of our IRAs invested in a high yield bond fund. It has averaged around 7-8% since the 2008 crash. Granted it's mostly invested in junk bonds, so there is a little risk, but it's been my "safe haven". Nate gave me a private education on how annuities have changed since I last looked into them. I still don't think they are for me, but it sounds like their structure has improved a bunch. I'm glad your's has worked out for you.

Matt

Stock markets tend to collapse when a crisis occurs. But I believe that it is not necessary to withdraw funds and stop trading at this time. On the contrary, the market becomes profitable again after the departure of weak players, and you can get superprofits during the stock price growth. I learned this on

https://www.earnforex.com/forex-e-books/, and this manner of behavior has already allowed me to earn hundreds of thousands several times. So I continue to stick to this strategy.

I am in my mid 70's invested since I was 29, and retired at 58. Yes I believe in the mattress fund, and standard savings etc, but the market, if your not too greedy, can make you money, it has for me,,,,,,,,

Although now, there is money to be made, there always is, but its up to you, to stay on top of it, know what you own, and have a relationship, with your advisor........

I am afraid, that Inflation is here for a few years. However I am surprised how little gold or silver, has increased in value, which puzzles me,,,,, They are both over sold, but some, in the portfolio does not hurt.

Our market has not "collapsed" really since 29. 87 and 98, were not good, but it did not collapse....... The inflation has been coming. Trump spent too much, in many ways, here comes the spend Commando Biden, and its exactly what we did not need. I knew once the stimulous checks were coming out, it was going to be trouble.....

Biden now has put it in the Federal Reserves' hand, except they are going nothing, and I do not see it at all. The Democrats have their head in the sand, still believing good job reports and wage increases are good, yet they refuse to adjust inflation.

Biggest cause of it all, is the war on fossil fuel. They want green energy, which is not going to happen, and you should just suck it up..... I do think, that they might have to make corrections. No reason we should not be energy independent. I see oil going to 115 a barrel by summer.....................................

I'm raising a little more cash from this current market rip today and tomorrow.

I don't advocate trading stocks........the tax consequences kill you. My son has been trading and he has had some huge gains in Moderna, [I think he said 400%] Pfizer, Nvidia, etc that he sold last year....but its funny to hear him talk about the taxes incurred from the sales. That Nvidia currently has a big fat covered call spread ....but I think the stock can be bought cheaper.

You can use the trading of losers and offset with some gainers to be tax neutral...or rotating from sectors you don't want to be better positioned. I think I can rotate into some good long term holds at a cheaper price later this year.

If not, then no sweat....I just get a mid single digit return in the meantime and I'm good with that while still holding a lot of cash. If the market dips, I buy some good stuff at a discount and hold it which typically results in big gains.

"I'm raising a little more cash from this current market rip today and tomorrow."

Which market did you see "rip" today? Did you mean "dip"?

Matt

Matt, it was up in the first couple of hours…probably due to so many being short…..then it dropped off a cliff.

Sagging more today. I cant predict the future…but typically markets drop more on interest rate rises…then recover some months later. A lot of that selling is in…its the selling for a huge Biden boo boo that Im worried about…and that can happen in multiple categories. I think the Odds are fairly high.

I am very glad that I have a good friend who always guides me in this field in order to not make stupid decisions because I don't understand it at all. He always tells me what and when to do it. I am more a gambler player but who knows the limits and I am very good at controlling myself so I don't lose a lot of money. Plus, I am playing only online on this site

https://wolfwinnercasino.com/ as it offers a lot of bonuses that are best for beginners and also has a fast withdrawal which is very important for me.

Its looked pretty damn rough for the last month in my opinion. But probably not for the stock geniuses in here.

Seeing as the vast majority of the money I have tied up in the market won't be touched for about 15-20 years at the earliest, a one month dip is of little consequence to me.

It looked rough in March of 2020. But you could either sell and cut your losses. Or buy more and make that much more on the way up. Just like buying land in a down market instead of selling in it.

Steve, I didn't believe you about the savings bonds so I looked it up. I had no idea they were paying over 7%. Makes me think we need to buy a bunch of bonds!

I’m screwed now, don’t want to invest in the market and real estate is ridiculous now. I’ll hang in to the cash and wait for the crash(hopefully just a slow down)

FYI.......S/P index up about 7% at the bell today from the start of this thread

FYI.......S/P index up about 7% at the bell today from the start of this thread

Bowsite makes the world go around!!!

Stix, that would have made sense when inflation rates were 2%. With 7-15% inflation your I bonds are worthless. This might change in a year if inflation gets controlled.

Not at all worthless dude if other options performing worse.

Always remember Pigs get fat and Hog’s get slaughtered lol Good luck Lewis

ibonds are only paying 7% because of sky high inflation so it is basically a zero percent return after inflation. the base rate actually is 0 and the rest is due to the inflation rate. you are also limited to buying 10k per year in ibonds and you really cant use them for current income.

In the 10 year period between 2011 and 2020, the S&P 500 averaged nearly 14% annual returns. During that same period I bonds averaged less than 3%. Using the current hyper-inflation period to advocate for I bonds as a long term investment strategy is a little short-sighted, IMO.

Matt

Lets look at the Tea leaves as I think there are a lot of buy the dip guys that have never been through a market cycle like this; 1) Gov posted inflation at 7.9%....last time it was that high 40 or so yrs ago the interest rates were 13%. 2) War 3) Political policy; Essentially we have an administration that is ignoring massive inflation and focused on other agendas. Thus, no solutions in sight. 4) Energy; The world is starting to realize we have been focused on Social issues and taken our eye off the ball- there will need to be some serious and expensive changes to right these wrongs of past policy. Point is, it will be a drag going forward. 5) Supply chain still mess and will be worse in the future due the the realization that counting on world JIT supply is a bad idea. Made in USA will be more important, but also more expensive. 6) many more problems; internet rate rises, Dollar devaluations, etc.

Goldman says its a 35% chance we will go into recession. With the Issues above, I don't see how its not 100% we go into recession. Currently its still buy the dip....when it should be sell the rip. It will probably take a year for the reality to take hold, then it will get progressively worse for the equity markets and small businesses. The companies with no earnings will of course get slaughtered.

Ask yourself; what happens when the folks that bought a home in the last 2 years suddenly have no equity?

Don't shoot the messenger.......

If you are going to panic at every down turn in the market then you shouldn't be in the market. No broker can time the market so i invest for the long term and it has worked really well for me. My average return on my vanguard portfolio over tens year from 2/28/12 is 13.60%. Five year return is 12.20%, 3yr return 14.10%, one year 8.30% What has me worried is that Biden and Harris are completely clueless and the Fed is now a joke.

Down turns create buying opportunities. Millions of dollars are to be made, for those willing to be in it for the long haul.

The markets have been on a nice bull run lately. They're only 5-6% below all-time highs, with lots of good buys still out there. I've been slowly adding positions to my portfolio, mostly value stocks with good balance sheets and plenty of cash, and pay good dividends.

"Be greedy when people are fearful......"

Matt

Asked above- “What happens when people that bought a house in the last two years have no equity in their house?” If they have/want to sell in the short term, they lost money. If not, they have a place to live, make payments and build equity. The alternative is rent and build equity for the owner of the dwelling.

Agreed on that Dale- this isn't the same signs as '08 in terms of housing crash, it may flatten out some but it's not going to drop by 30%. The dollar is worth less, people are still fighting at the bit for property and banks are not giving out loans to McDonald's workers for million dollar vacation home at subprime rates. It's an apples to oranges comparison.

Inflation is rampant, so someone that bought their house 2 years ago will have more equity, they're paying for an asset with less valuable money than when they locked in that mortgage 2 years ago.

I'm continuing to lock in cheap debt on income producing assets while still slugging away at the stock market. I'm in for the long haul while keeping enough cash liquid.

"Prior to retirement in 2018 I was 100% in the market. The gains enabled me to retire at 55. Since retirement I'm totally out of the market, and heavily into Series I bonds. They're now paying around 7.5%. I could have made alot more if I stayed in the market, but I dont need it and I'm content, and living well."

I retired last year at 51 and my money manager at Morgan Stanley cautioned strongly against the traditional investment advice of re-balancing one's portfolio away from equities and towards bonds for early retirees. His thesis is, while may have been sound advice for people who were retiring at 65 and only expecting to live until 80, it could potentially result in people who retire at 50-55 and live to 90 running out of money prior to their deaths.

In terms of liquidity, we are ~98% in equities although we have shifted a bit more toward value/dividends than growth.

As stated above, generating a 7.5% return today is flat/negative once inflation adjusted.

I'm 36 and planning to retire at 55 God willing. Putting 15% into retirement, working on paying off the house next. Only challenge will be we were blessed with a special needs child, and its tough to determine what support she will need as she grows up. We have an ENABLE acct set up for her now to help in the future for any large issues, but for now we cashflow any expenses.

Good for all you that retired when you wanted and could!! If you have solid advice outside what my wife and I are doing I'd love to hear it!

We are entering electric vehicle and electric energy storage age. My advice is to invest in Tesla, but regardless of your investments just remember time in the market consistently beats trying to time the mark - this has been back tested over and over again and is not one man's pet theory. It does require intestinal fortitude certain years. Any serious investor at whatever stage you are in of your life needs to understand the power of compounding interest. Google "Einstein's Eighth Wonder of the World". When you get your investment snowball growing exponentially, it is a beautiful thing...

My only thought is, in this current high inflation environment, I would not pay down cheap mortgage debt any faster than required. Put that money into equities. When inflation is approaching double digit rates and your mortgage interest rate is likely 3-4%, delay paying that back now and use inflated future dollars to do so.

"Any serious investor at whatever stage you are in of your life needs to understand the power of compounding interest."

Worth repeating ^^^^^

Historically, the stock markets have averaged around a 10% annual return (not adjusted for inflation). With compounding interest, that means your stock investments should double every 7 years, without adding any principle. So, under normal market conditions, a $10K investment today would be worth $80K in 21 years. If you periodically add to your investments, your nest egg grows even faster. Exponential growth is truly a wonderful thing, especially if you start investing early in life.

Matt

Agree with Matt on not paying off cheap debt when those extra payments could be invested instead. I don't care what Dave Ramsey says.

And by all means make sure you have a high ESG rating!

Good point on the cheap debt part. To be honest, I cant stand having payments, yes a bit Dave Ramsey thoughts. I max out 401k and IRAs, what else can I invest in for retirement?

Chubbs, think of those "payments" as low interest investment contributions. I took out a reverse mortgage on one of my houses six years ago, used the money to supplement our income for a few years before a big annuity and Social Security kicked in. It was not taxable and kept my reported AGI just above poverty level to qualify for basically "free" Obamacare until I could get Medicare (Hey, I didn't make the rules...). Plus, I could keep my investments intact and rolling through the bull market.

Now, I could easily pay off the balance and not make a big dent in the portfolio, but at 2.4% interest, it makes no sense. It's cheap money that won't come due until I sell the house, and with the real estate market so hot here, my equity is far outgaining the interest accruing on the balance owed.

^^^^ Also known as leveraging debt.

Matt

We did the whole Dave Ramsey thing several years ago, went to the studio to do the "debt free yell" and literally bought the tee shirt. In fact my wife still carries her envelopes with cash. I don't agree with everything he preaches but he is spot on about being debt free, there's nothing like it. We were in our 30's with zero debt including the house, maxing out retirement accounts. Seven years ago we moved and wrote a check for our current home, pretty cool feeling. A couple of years ago I did the unthinkable and took a cash out mortgage on the house to buy 50 acres for hunting. It was a good buy in the exact right spot and it is already worth a lot more than we paid for it so it has turned out to be a good investment. But now I have a mortgage again and I can't stand it, even at 3.5%. We have backed off retirement savings to pay off this loan ASAP, nine months to go to be back in the black. I know that financially it would make more sense to be plowing this money into the market, but I won't stop until it's paid off. Plus, we already have a good amount compounding in the markets. That's my perspective on "cheap" debt.

Mutual funds up from this time last year. Oil stocks you can't loose on, just about ever. Wish I had more oil stock!! With the war and U.S. looking to send natural gas off to europe to replace Russia NG, I say that going to look good also.

The only two stocks I can think of I ever lost everything I put into them were oil stocks. A couple smaller companies but publicly trade. My Father in Law was bitching about the money he had lost in them when oil prices fell. I thought now the time to buy them while they are down. Oil prices did not come back up but stayed low and neither recovered and went bankrupt. Luckily I only bought a few thousand between both of them. Point being you can loose on oil stocks. Not saying don't buy them just lots of diversification.

My two big losers - Penn West, an Alberta oil production company that was once one of the 60 largest companies on the Canadian stock exchange. Totally tanked. Now owned by Obsidian Energy.

The other was a hot tech company I joined in 2000 at the peak of the tech boom. Tellabs. It had the 4th best performing stock of the decade of the 90s (behind Cisco, Dell, Intel). Admin assistants were driving Maseratis after multiple splits. Then WorldCom collapsed (our biggest customer), most of the tech sector collapsed, the stock, and my options, went from $77 to $3 almost overnight. What was a $2B+ annual revenue company now no longer exists.

My biggest loser, recently, has been a Cathy Woods managed ETF. I bit on all the hype after her 3 ARK funds produced the highest returns of any during the Covid market recovery. I bought near the highs a year ago, now I'm currently down about 50%. It's only a loss if I sell, so I'm holding and hoping it recovers. Fortunately, it's a relatively small investment. It's been one of those "if it sounds too good to be true..." type lessens.

Matt

" It's only a loss if I sell, so I'm holding and hoping it recovers."

Matt, I gave that rationing up long ago. I'd get the hell out and put the $ in something that's positive. JMO

Dan, I hear you. I just hate pushing the sell button when I'm in the red this far. It's a very small percentage of my portfolio, so it's not a big difference maker either way. But you're right, I should have dumped it long ago.

Matt

Thanks for the advice guys.

I had some Disney Stock in my IRA that I sold yesterday with a big gain. I think they are committing suicide going woke otherwise I wouldn't have sold.

It's great to hear from you, Dan

It sounds like we have similar investing styles. I have my "fun money" account that I "swing trade" with, then we have our retirement accounts that are more long term. I rarely touch them.

There's definitely an addictive quality to trading stocks. I started dabbling with options a few years ago, but quickly decided that was a little too much "action' for me. LOL!

Matt

Nice to see you post Blue! Hope all is well up Nort.

Thanks Norse..... been a hard long winter for an old man. Still haven't quite shaken that dang Lyme disease crap it seems. Did not even get on the ice this year. :( But...getting by.

Dan, using a moving average for stops is a good idea, but it seems like a lot of work. Can you automate that, or do you set new stops daily?

Matt

I used to set stops daily, too. Then in Sept of 2020 I went on a month long elk hunt. Before I left, I set stops at a fixed percentage below the current share prices. You may recall, the markets had a short-lived correction of about 10% that month, then climbed right back up. Over half my portfolio sold off, while I was chasing elk. The taxes on that mistake stung a little...LOL! So, I'm still searching for a method that doesn't require daily input, too

Matt

Matt, I say your elk hunt stops worked perfectly. The market reversed and went up but it didn't have to. I think any stop is gonna get whipsawed sometimes. But it's priceless insurance.

It's been hard for me to go this way but I'm pretty sure for me it's the way to go.

Matt, if you hadn't been on a hunt would you have changed your stops?

Just my opinion...if you're gonna change your stop because it's gong to be hit, why'd you set it in the first place?

Still learning and hopefully always will be.

Dan, yes, I would have changed the stops on a few positions with healthy short term gains, for tax reasons.

Matt

I think we will look back on 3.25% mortgages in a few years and see it was a no brainer.

Bluedog, thx for posting…interesting. Is there an indicator in your system that would have you increase the $$ devoted to a trade?

bluedog, first of all thank you for your service and second for your advice along with others such as Grey Ghost regarding buying stocks. Had I known to do what you guys are saying maybe I would have avoided the complete loss of my Enron stock back in 2001. Badbull

beendare...not really, I've been know to increase a holding but lack records to show + or - results.

badbull...... I had my own disaster around your Enron time.. I'd run my account up over 450k with what I recognized as very dubious valued internet crap. I was 10 foot tall and bulletproof no stops. No skills and really a total FNG... I'd just sell when market turned. Then the fickle finger of fate threw a knuckleball. I got stupid and did a compound skull fracture, mri showed 2 brain tumors previously unknown .. anyway after surgery and gamma knife..maybe 8, 9 months later I'd come around enough to remember I owned stocks. After logging in my fat 450k was down over 95%. Yup.. fk me. LOL Should write a how not to self improvement book.. How to turn 450k into 18k.. lord , makes me nauseous just remembering, try to block it from memory.

Guess education isn't free.