Replacing Cabela's card. Best option?

General Topic

So my Cabela's card was hacked yet again and I understand they will be replacing everyone's card shortly as part of the BPS deal. I don't really care for the rewards program any more because I don't really want anything from Cabela's any more. I used to buy boots and clothes from them but their quality and selection of tall clothes has really gone to Hell.

So, I am looking for advice on good choices to replace it with. Rewards programs, etc. Something that benefits hunting/conservation would be a bonus. What are you guys and gals using?

I just use my usaa card. Gives me the same cash back as cabelas right into my checking account. Also have their American express that gives me 5% back on gas and groceries. Like you, I don't buy much from cabelas any more.

With an Amazon card, the rewards are pretty good, and we get to determine what organization gets a percentage of our purchases.

I haven't seen the Amazon card. What are the rewards?

From: skookumjt 04-Aug-18 I haven't seen the Amazon card. What are the rewards?

I just deep sixed my Cabelas card and will now use my Amazon card for everything, as it's as good or better than the Cabelas Visa card I just closed out. Check it out on the web, as that's what I'd also suggest you go with.

Rocky Mtn Elk Foundation has a rewards Visa through Commerce Bank in KC. You can learn more about it at the RMEF web site

BOA and Rewards card and which ever AMEX card works best for your needs.

If you live in or travel to Alaska a lot the Alaska Airlines card is a no brainer.

I fly enough that it’s the only card I use for simplicity.

I use a Southwest Visa. I get free plane tickets all the time.

+1 ohiohunter. Get a card you can make 2% on everything you buy and use it for all your everyday purchases. Pay bills with it if you can. Just don't carry over a balance. It really adds up and you can spend that money anywhere you want!

I can't see using anything but the 2% cards that are available now. Cabelas are 1% a can only be used at Cabealas/BPS. Double that and can be used anywhere they take Visa. I have to spark visa car and use it for business. As stated, if you don't pay it off every month, you lose more than you gain.

What are the 2% cards being referred to?

See ohiohunters post above.

I cut up my credit cards.

You can actually hurt your credit rating by closing cc accounts. If it doesn’t have yearly fee, just put it away and don’t use it.

To score high in credit, it’s best to revolve a couple cards every 3-4 months. Make somes charges and then go back to your main cc.

For those with the Amazon Visa, is it the Prime or Signature card? 10% of the reviews are bad. What’s your experience?

I dont care about credit score. I dont borrow money so I see no need to keep a high score.

Isn't Citibank anti-gun or anti-hunting ? Seems to me I read that a few years ago. I could be wrong, I was once before....

Trial: BOA is one of a cartel tyring to bankrupt the firearms industry.

Go to nerd wallet and look at the compare cards. Youd br hard pressed to get a 2% avg. Not over a broad range of purchases...not happening.

I get more than 2% in value on dollars spent with my airline miles card. Specified use for sure, but I spend enough on airfare each year that it’s a nonissue

cnelk is indeed correct you can hurt your credit rating by cancelling your credit cards. As stated if NO ANUAL fee I just put them in the safe and forget about them. I will be cancelling my Cabela's CC very soon also. Store selection really suck as do their prices.

If you do a lot of out of state hunts you can find cards for certain airlines to help pay for the trips. Or Amazon.. Amazon is a solid option I buy too much stuff from there.

I was going to say, if you fly then either Alaska or SW is a no brainer...

KSgobbler, I am in same situation. Have not paid a penny in interest or borrowed money in years. So I thought credit score was a non issue. Recently I changed insurance companies. My insurance agent ran a credit score on me and said my very good credit score lowered my premiums. I did not know about that before she told me.

I’d definitely be more concerned about my credit score than the weight or speed of my arrows

Who wouldn't want 2% cash back on everything you buy or travel miles for guys like TEmbry?

By far the best way to earn miles or points is in getting the introductory incentive bonus when you sign-up for a new credit card. Example: If you spend 5,000 on your existing card, even if you get double points, you end up with somewhere between 5,000 and 10,000 points. But, you can spend less than that on a new card and get 50,00 or more points as an introductory offer. On the attached link, you could earn $78,000 miles by only spending $3,000!

Those that feel like they have to stay with one card their entire life are missing out on a lot of opportunity! If you might be ready to apply for another card, here’s an OUTSTANDING offer from AMEX for Delta Skymiles (Delta miles never expire). With this link they’re letting me refer people to an AMEX card and receive over 75,000 miles (the regular sign-up bonus for this card on their website is only 35,000 miles) after spending just $3,000 in 90 days! I have no affiliation with AMEX or Delta, but I will get a few miles if you sign-up with the link (but it's anonymous, so I'll never know who applied). But I mostly just like to help fellow hunters take advantage of these great benefits like I do. I've had many a great free flight this way!

This year, round trip flights to Africa started at 90,000 miles, which would have cost over $2,000 if paid in cash. Of course the miles could be used to fly anywhere. I just pointed that out to show you the value of this amount of miles you would earn. If for some reason you didn’t have enough miles to buy a flight you wanted, Delta also allows you to pay with a mixture of miles and dollars. By the way, Delta frequent flyer miles NEVER EXPIRE, so you will always have them available whatever year you decide to book a trip (but the offer to earn this many miles will expire). Also, if there is even one seat left on a flight, you can buy it with miles. There's no limit on how many free seats are available on each flight like there is with most airlines.

There’s a $195 annual fee on this card, but that is a small amount to pay to bank that many points that never expire! You can also effectively get some of that fee back, since you can also get a $100 statement credit with this offer if you spend at least $1 on a Delta purchase during the 90 day period. You can buy a bottle of water or some earbuds if you are flying on Delta soon, but I usually just go online and buy a Delta gift card from their website for $50. I then own a $50 Delta gift card that never expires, and I receive a $100 credit to my bill which pays half the annual fee amount.

This card also gives you a free companion pass good for any Continental US flight each year you renew the card, which more than pays for the annual fee if you use it (or you can sell it to another AMEX holder, since the only requirement is that the first ticket is purchased with an AMEX card to get the second one free). You can your buddy could fly to a hunting convention for half price each.

This is a great offer, but I think it only last two weeks and then it’s gone. I don’t think I’ve ever seen a better offer on this Delta credit card, so I would highly suggest jumping on it if you’re in the market for another card!

I use mainly a Fidelity Visa that deposits 2% cash on all purchases directly into my brokerage account the end of each month. Bank of America for 3% back on gas. Discover for whatever they are giving 5% back on that quarter. Have never paid an annual fee on any card and no plans to. Also never card hopped - too lazy. Avoided airline miles cards or cards that tied me to one place - give me money please. With Fidelity, if I don't want to use my 2% refund to buy stock, I can sweep the money into my checking account with no charges. Comment above absolutely correct about your credit score affecting your insurance rates, so it will save you money to keep as good score as possible (at least over 720; over 800 even better). With online payments (and without the vagaries of the US Mail), I pay all of my balances in full the day before they are due, giving up to 6 weeks of float for free. No real monetary value, but it somehow feels like a win. Most important of all is to not carry any unpaid balances, ever. Even 5% cash back won't be much help if you're paying 24% interest on an unpaid balance.

Scheels card. Use it for everything, then earn gift cards.

No Mercy, why only earn 1% back that you can only spend at Scheels when you could earn 2% back that you can spend anywhere? Check out the Citi card.

Ahh the old credit score. The badge of stupidity also known as the gateway to things you can’t really afford.

I've been very happy with my Amazon Prime Visa/Chase card.

Good luck, Robb

"Ahh the old credit score. The badge of stupidity also known as the gateway to things you can’t really afford."

Huh?

I think he’s referring to the weak minded credit card holders who don’t use them as debit cards, keep them paid off, and get free incentives.

I personally see credit cards the opposite way, I think people who DONT use them are the stupid ones. Giving away free money/flights/etc.

Agree, Trevor. Other benefits as well like purchase protection.

I bought a trail cam put it out. Bear chewed it up. Use extra warranty on credit card that most people don't even know they have, bam, new trail camera paid for. Same with my installers ipad that he dropped a 2x4 on. If you've got a decent card, chances are you've got some awesome extra purchase warranties, car rental insurance etc etc. Besides the obvious incentives like money back. Besides the fact that if someone hacks it they won't stick you for anything.

Unless someone has an issue with over-spending on a card, I do not see the reasons to put absolutely everything on a card. If you can't manage money that way, then don't. But if you can, why wouldn't you.

APauls,

"...I do not see the reasons to put absolutely everything on a card."

I think you meant the opposite of what you typed. I think you meant to say that you see no reason why people should NOT put everything on a credit card, for the reasons you mentioned in your post. I agree. Unless a person has no self control when they own a credit card, there are a world of benefits in using a credit card over a debit card, including security and extended warranties. And except for the same reason, there's no real reason to only have one credit card unless you don't trust yourself. Different cards are best for different things. Having several cards actually increases your credit rating, all things (including total monthly spend) being equal, because you are using a smaller percentage of your overall available credit each month.

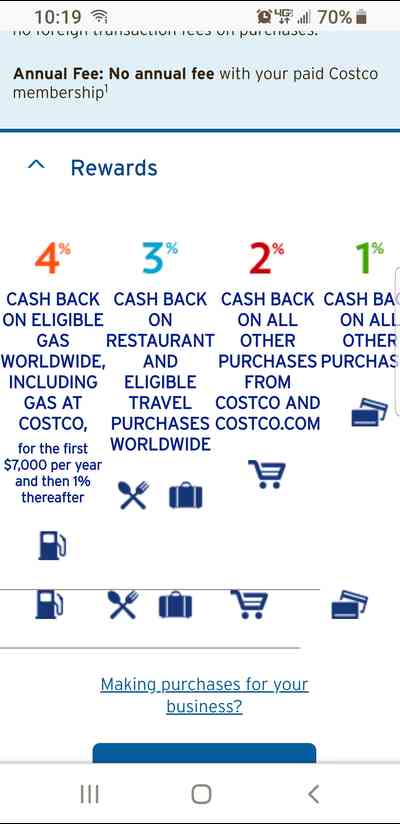

How would you guys rate this Costco CC?

I think "best" depends on what you want. For years wife and I had a card that gave us "points" you cashed in essentially on gift cards, we would use the points to get cards for a restaraunt we frequented, so essentially we'd get free meals.

Now we've moved cross-country and are more interested in travel, so we debated between United Airlines (only flight option to us) or Capital One, we went Capital one after doing side by side comparison. The benefits over united: no blackout on flights (essentially you buy the ticket, then refund yourself, so United doesn't see it as a free miles used flight), and 2x "miles" on everything vs United had 1x miles on non travel/hotel purchase. The downside with United, aside from blackouts was changing mileage usage, but they had free checked bag. The only upside to united vs capital one is a with United a flight is a flight, all equal on miles checked, vs Capital One you pay for the ticket so could cost more/less at times. United is changing the "all flights equal miles" this November which made us nervous. Since Boston is our target destination, that would probably be a "desired flight" so would be more miles

My wife has an rei cc. Pretty good.

This is a dumb question, but you are not charged interest as long as you pay off the balance in full BEFORE the due date, or on the day it's due?

On the day that it's due. Put it on an automatic payment on the due date for the statement balance and you'll never pay a dime of interest.

Amazon rewards pretty sweet.